The S&P Healthcare Services Index decreased 0.5% over the last month, as compared to S&P 500, which increased 0.1% over the same period.

Over the past month, the sectors experiencing the most growth were Providers – Rehabilitation (up 6.7%), Healthcare Staffing (up 5.8%) and Dialysis Services (up 5.4%). The sectors experiencing most decline were Commercial Managed Care (down 7.9%), Consumer Directed Health / Wellness (down 6.8%) and Assisted / Independent Living (down 6.3%).

The current average LTM revenue and LTM EBITDA multiples for the Healthcare Services industry overall are 2.8x and 15.8x, respectively.

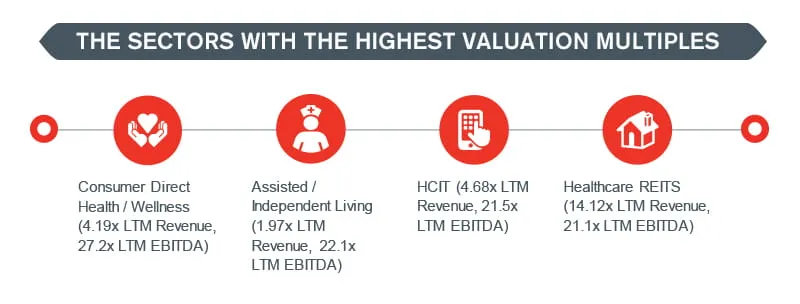

The sectors with the highest valuation multiples include:

- Consumer Direct Health / Wellness (4.19x LTM Revenue, 27.2x LTM EBITDA)

- Assisted / Independent Living (1.97x LTM Revenue, 22.1x LTM EBITDA)

- Healthcare REITS (14.12x LTM Revenue, 21.1x LTM EBITDA)

- HCIT (4.68x LTM Revenue, 21.5x LTM EBITDA)

Read the report for more detail on sector activity.

Source: S&P Global Market Intelligence as of January 31, 2020, and includes the most actively traded healthcare companies for respective covered sectors, excluding most microcap companies.