The S&P Healthcare Services Index increased by 14.3% over the last month, compared to the S&P 500 Index, which increased 10.8% over the same period.

Over the past month:

- The sectors that experienced the most growth were Assisted/Independent Living (up 42.2%), Providers – Other (up 36.5%) and Consumer Directed Health/Wellness (up 30.8%).

- The sector that experienced the largest decline was Home Health/Hospice (down 1.4%).

- The current average Last Twelve Months (LTM) revenue and LTM EBITDA multiples for the healthcare services industry overall are 1.82x and 10.1x, respectively.

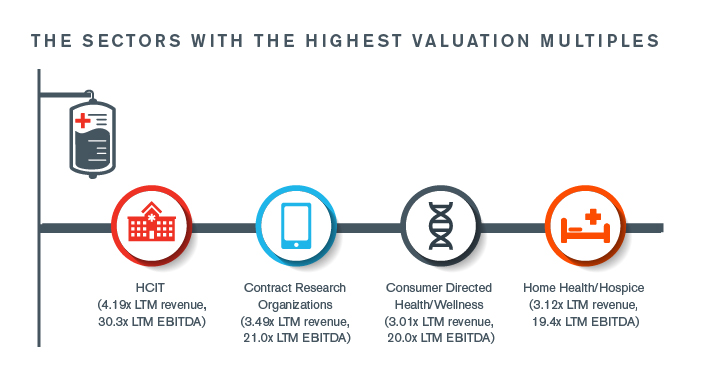

The sectors with the highest valuation multiples include:

- HCIT (4.19x LTM revenue, 30.3x LTM EBITDA)

- Contract Research Organizations (3.49x LTM revenue, 21.0x LTM EBITDA)

- Consumer Directed Health/Wellness (3.01x LTM revenue, 20.0x LTM EBITDA)

- Home Health/Hospice (3.12x LTM revenue, 19.4x LTM EBITDA)

Stay Ahead with Kroll

Distressed M&A and Special Situations

Kroll professionals have advised hundreds of companies, investors and other stakeholders at all stages of distressed transactions and special situations.

Transaction Advisory Services

Kroll provides comprehensive due diligence, operational insights, and tax structuring support, assisting private equity firms and corporate clients throughout the deal lifecycle.

Transaction Opinions

Our Transaction Opinions solutions span fairness opinions, solvency opinions, ESOP/ERISA advisory, board and special committee advisory, and complex valuations.

Financial Sponsors Group

Dedicated coverage and access to M&A deal-flow for financial sponsors.