In a recent article on the economic impact of COVID-19 on pending M&A transactions, we discussed how COVID-19 may serve as a trigger for parties seeking to terminate a transaction under an MAE clause. We described four quantitative analyses companies should perform to prepare for a potential MAE dispute. In this article, we turn our attention to those transactions that have successfully closed and where the parties are working to resolve another customary feature of an M&A transaction—the post-closing determination of the target’s closing working capital as of the closing date and any associated purchase price adjustments.

In light of the uncertainty deriving from COVID-19, we fully expect that such a determination will become a much more challenging exercise. Working capital disputes can be contentious in the best of times, but in this period of global economic upheaval, there likely will be an even greater chasm between a seller’s pre-closing estimate and a buyer’s post-closing true-up of working capital.

The key to determining any impact of COVID-19 on the target’s closing balance sheet will be the timeline between the transaction closing and subsequent true-up of working capital in relation to the evolution of the COVID-19 financial and economic crises and its impact on the acquisition target. U.S. GAAP and IFRS provide the relevant guidance that preparers of financial statements must consider when measuring any impact of COVID-19 on a target company’s closing balance sheet. In particular, the FASB’s Subsequent Events guidance, found in ASC 855 and IFRS’ IAS 10, will be pivotal for performing working capital true-ups in the COVID-19 era.

ASC 855 provides that subsequent events and their effects should be recognized in financial statements when there is evidence that conditions existed at the date of the balance sheet (i.e. the fiscal reporting period end date). The recognized subsequent events should provide additional evidence about the conditions that existed as of the balance sheet date and should be considered at the financial statement issue date. For example, ASC 855 reads, “a loss on an uncollectible trade account receivable as a result of a customer’s deteriorating financial condition leading to bankruptcy after the balance sheet date but before the financial statements are issued or are available to be issued ordinarily will be indicative of conditions existing at the balance sheet date.”1

While closing working capital is not specifically identified within the subsequent events guidance, ASC 855 is commonly applied when determining the post-closing time period for which information may be considered in preparing financial statements that are used to derive closing working capital. Analogous to the date when an entity’s financial statements are available to be issued, the true-up date is when the calculation of transferred working capital is determined.

Under a GAAP- or IFRS-specified basis of preparation, working capital is derived from a balance sheet limited to accounting for those conditions that existed at the closing date but which are informed by additional information learned through the date of preparation of the financial statements that reflect those conditions (i.e., the true-up date). This methodology is similar to identifying the conditions that existed at the fiscal reporting period end date and assessing the significance of subsequent events on those conditions, before the financial statements are issued. ASC 855 defines these post-balance sheet subsequent events as Type 1,“recognized” (or “adjusting”) events. By contrast, Type 2,“non-recognized” (or “non-adjusting”) subsequent events either inform conditions or are conditions that did not exist at the balance sheet date and do not affect account balances and therefore would not be recognized for purposes of a post-closing working capital calculation.

With respect to the financial and economic fallout from COVID-19, the distinction between these two types of subsequent events will require the financial statement preparer to determine the date on which the pandemic became a condition affecting the target company in relation to the transaction closing date. This will determine the extent of the pandemic’s impact on closing working capital, if any, and the significance of information learned through the true-up date.

The parties will need to consider many facts and circumstances in any such analysis. Two of the most important variables that will determine the designation of COVID-19 as a recognized or non-recognized subsequent event are:

- the geographic location(s) of the target’s business operations and its customer base, and

- the industry/industries in which the target operates. It is clear that the financial and economic dislocations from COVID-19 have affected different parts of the world at different times, and that these impacts have affected certain industries more severely than others.

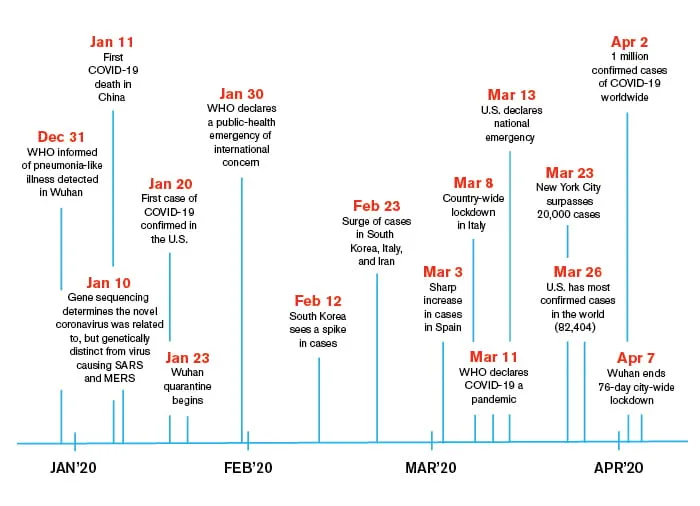

The following timeline provides a high-level overview of certain key dates in the evolution of the COVID-19 pandemic:

Although the biological and geographic origins of COVID-19 remain the subject of debate, a hypothetical example is instructive. Assume that a target company in the manufacturing industry was acquired in a transaction that closed on January 31, 2020 and for which the working capital true-up was scheduled to take place 45 days later, on March 16, 2020. Further, let’s assume that the company’s manufacturing business was for a non-essential product for the leisure industry. In this hypothetical, the target company has a significant manufacturing presence or customer base in China and, based on the timeline above, there appears to be evidence that COVID-19 was a condition that existed as of the closing date.

Accordingly, any information that assists the financial statement preparer in refining estimates for uncollectible receivables reserves or the net realizable value of inventory would be considered a recognized subsequent event and should be considered in the true-up of working capital at the agreed-upon date. If we modify the hypothetical to assume instead that the target company’s operations are located entirely within the U.S. and the company exclusively serves a domestic customer base, it is more likely that the COVID-19 pandemic would not be considered a condition that existed as of the January 31, 2020 closing date. Under this hypothetical fact pattern, COVID-19 would represent a non-recognized subsequent event that would not result in an adjustment to the closing balance sheet because it was not determined that the impact of COVID-19 had reached the U.S. as of that date. As the above timeline shows, the clarity surrounding this type of accounting judgment is obscured for transactions that closed in February and early March for companies similar to the U.S.-based company in our hypothetical.

Consequently, the timeline for determining whether financial and business dislocations attributable to COVID-19 will be considered a recognized or non-recognized subsequent event for a target company is directly related to when COVID-19 was a condition affecting the acquisition target and, therefore, is not subject to one-size-fits-all analysis.

Each key event in the evolution of COVID-19 is a separate occurrence (e.g., the initial outbreak in Wuhan, WHO declaration of international public health emergency, WHO declaration of worldwide pandemic, enactment of containment measures and announcement of government aid), and will impact different businesses at different times with varying levels of severity. The ultimate determination of whether COIVD-19 was a condition that existed as of the closing date will depend on the facts and circumstances impacting the target company and will require accountants and business leaders to apply professional judgment in making that determination. As such, judgments that impact post-closing working capital adjustments, such as whether to book an increased allowance for bad debt or whether to write off potentially obsolete inventory, will become the subject of scrutiny by buyers and lead to disputes.

Additionally, for those preparing working capital calculations that include financial assets and liabilities, though rare, one will also need to consider the impact of COVID-19 disruptions on fair value calculations. For financial instruments held at fair value it is important to understand what level of inputs are being used (i.e., Level 1, 2 or 3).2 For those using Level 1 or 2 inputs, fair value should have incorporated all of the information and uncertainties to be considered at the date of measurement (because they are observable), and there will typically be no adjustment required. For those using Level 3 inputs, an entity would be required to adjust the carrying value if reasonably available information indicates that other market participants would have used different assumptions at the reporting date. In circumstances such as these, preparers must apply judgement without use of hindsight.

Lastly, for those assets or liabilities measured on a basis other than fair value, material developments that provide the preparer with additional information relating to reasonably expected impacts of COVID-19 at the balance sheet date would result in an adjustment. As such, the impact of COVID-19 and subsequent events should be among the factors that preparers considered at the balance sheet date.

Duff & Phelps is a leading provider of expert accounting, valuation consulting, neutral arbitration and testifying expert services to companies facing post-closing purchase price disputes. We help corporates, venture capital firms and private equity funds with matters ranging from routine negotiation of post-closing differences to resolution proceedings administered by our neutral accountants to formal arbitration hearing and in-court litigation. Our forensic accounting, transactions and valuation professionals are deeply experienced in providing analytical support in negotiations, as neutrals, or in arbitration or litigation relating to post-closing working capital adjustments, including, but not limited to, the following items:

- Application of FASB’s Subsequent Events guidance, ASC 855

- Assessment of compliance with the appropriate basis of accounting preparation, including U.S. GAAP, IFRS, consistent practice, contractually specified and/or other applicable guidance

- Consistency of applied policies, practices and methods across the relevant measurement period

For more information on this and other M&A-related questions facing your business, please reach out directly to our M&A Post Acquisition Disputes team.

Sources

1 Financial Accounting Standards Board Accounting Standards Codification 855, Subsequent Events (“ASC 855”).

2 Financial Accounting Standards Board Accounting Standards Codification 820 ("FASB ASC 820") Fair Value Measurement (and International Financial Reporting Standards 13 ("IFRS 13") Fair Value Measurement) define fair value as a measurement determined by the assumptions that market participants would make in pricing an asset or liability. This statement establishes a three Level hierarchy of fair value measurement based on data assumptions and inputs. Levels 1 and 2 are assets with observable and measurable inputs available in the market, (i.e. quoted security prices), while Level 3 represents assets with unobservable inputs requiring subjective assumptions to be developed and applied.