For owners of listed and historic buildings in the UK, insurance valuation is rarely straightforward. Too often, reinstatement sums are based on assumptions, generic rebuilding rates, loan or mortgage valuations, none of which reflect the real cost of reinstating a heritage property after a serious loss.

Listed buildings can be found in various uses: hotels, shops, education, residential, pubs, and offices. The result is widespread underinsurance, across all sectors, discovered only when it is too late.

An expert valuation, carried out by specialists who understand both historic construction and insurance requirements, is not a luxury. It is essential risk management.

Wills Memorial Building, Bristol

The Fundamental Problem: Listed Buildings Do Not Behave Like Modern Buildings

A modern brick house may be relatively predictable to reinstate. A listed building is not.

Historic and listed properties often involve traditional materials and construction methods, specialist trades, longer programmes, conservation approvals, statutory controls, higher professional fees, site constraints and restricted access.

Yet many insurance sums insured are still derived from mortgage or loan security valuations, online rebuild calculators, or standard rates intended for modern buildings. These methods systematically underestimate risk.

Market Value, Mortgage Value and Insurance Value Are Not Connected

One of the most persistent causes of underinsurance is confusion between values.

An insurance reinstatement cost valuation is not a market value, is not a mortgage or loan security valuation, and has no correlation with what a buyer would pay. It represents the total cost to reinstate the building following a total loss, including demolition, professional fees and statutory compliance.

For listed buildings, that figure is frequently far higher than standard modern rebuild assumptions.

Why Generic Rebuild Rates Fail for Listed and Historic Buildings

In 2026 a question posed online to ask the rebuild rates for a brick building suggested a typical rate of between £1,000 to £3,200 per m2. If followed, this guidance could be dangerous as £1,000 per m2 is below the current lowest rebuild rate per m2 that we would be recommending. In addition, any range that is broad will depend on many factors. It is concerning that people may rely on such information and opt for lowest rate, leaving them in a position of underinsurance. In practice, listed properties frequently exceed the upper end of this search, and by a substantial margin.

This is due to the use of traditional materials, specialist conservation contractors, bespoke joinery and finishes, slower construction methods, higher preliminaries and extended programmes. Where a property is architecturally complex or contains significant historic fabric, reinstatement costs can increase dramatically once professional fees, contingencies and approvals are properly accounted for.

Hidden Cost Drivers That Are Often Missed

An expert insurance valuation considers cost drivers that are routinely excluded from informal estimates.

Specific Location Factors

Older buildings are often located in the heart of a town or city. Access to them – compared to when they were built – is now often very complicated. Narrow streets, restricted parking, bus lanes and adjacent exposures, including other listed buildings and critical infrastructure such as a railway station, can all increase the rebuild cost.

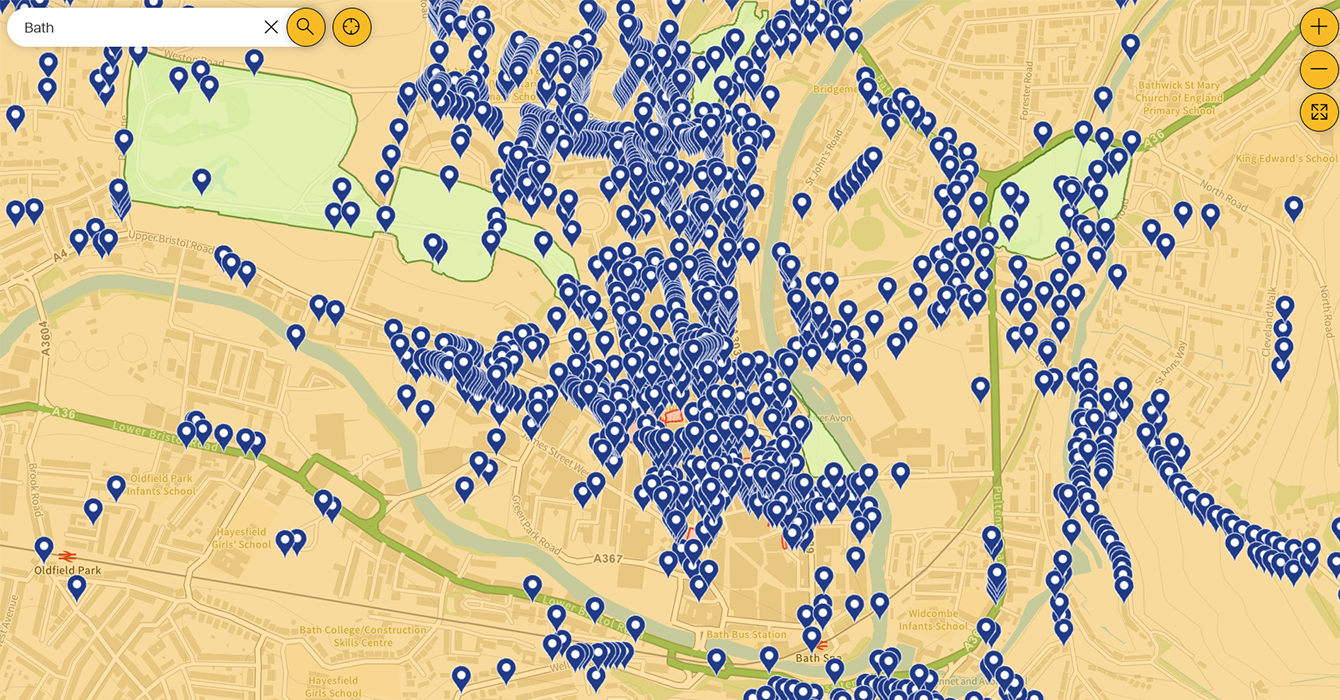

This is a Snip From Historic England Website Showing the Concentration of Listed Buildings in Bath. Every Marker is a Listed Building

Real Buildings, Real Losses

In March 2026, the enormous fire that engulfed a Grade B listed building adjacent to Glasgow Central Station, leading to its total collapse and impacting critical infrastructure and adjacent property, demonstrates a number of facts discussed in this paper: it is possible to have a total loss, stone does burn, the intensity of a fire can lead to structural collapse and the city and town centre locations of many listed and historic buildings adds to the complexity of any reinstatement cost assessment.

Forsyth House (Grade B Listed) in Glasgow City Centre Before the Blaze of March 2026 Caused Partial Collapse of the Building

Professional Fees

Listed buildings often require a broader and more specialist professional team, including conservation architects, engineers, heritage consultants and planning specialists. Fees may represent a significantly higher proportion of rebuild cost than for a standard building.

Stone Mason Working on the Renovation of an Old Building

Time Delays

Reinstatement of listed buildings commonly takes longer due to conservation consent, specialist contractor availability and statutory conditions. Extended programmes increase preliminaries and expose projects to inflation risk.

Conservation Approvals and Materials Risk

Local authorities and statutory bodies may require original construction methods or materials to be replicated. In some cases, sourcing matching materials can be uncertain or costly, and the extent of works may only become clear once construction begins.

A Sculptor Carving Stone

Complexity, Curtilage and Outbuildings

Listed or heritage status frequently extends beyond the principal structure to include boundary walls, ancillary buildings and structures within the historic curtilage. Failure to include these elements can materially understate reinstatement exposure.

Aerial View of Historical Buildings in Oxford, Uk

Why Insurers Rely on Expert, Defensible Valuations

From an insurer’s perspective, the issue is not simply the premium but claims defensibility.

Inadequate sums insured can lead to the application of average, coverage disputes, delayed settlements and reputational risk. An expert reinstatement valuation provides a clear and auditable rationale for the declared value, reducing uncertainty at the point of loss.

The Role of the Fixed Asset Advisory Services (FAAS) Team at Kroll

The FAAS (Fixed Asset Advisory Services) team at Kroll brings together technical understanding of complex assets, experience supporting insurers, brokers and property owners, independence and analytical rigour.

For listed and historic buildings, this combination is critical. An effective insurance valuation must bridge heritage construction knowledge and insurance valuation discipline.

A Valuation That Works When It Matters

The real test of an insurance valuation is not when the policy is placed, but when a loss occurs.

An expert valuation helps ensure the sum insured reflects real reinstatement risk, claims proceed without unnecessary dispute, owners are not left funding shortfalls themselves, and insurers can respond with confidence.

Speak with a Kroll Expert

If you are responsible for the insurance of a listed or historic building, whether as an owner, trustee, broker or adviser, an expert reinstatement valuation is one of the most important risk decisions you will make.

The FAAS team at Kroll can provide independent, defensible evaluations tailored to the unique challenges of heritage property.