The April note asked in its title “Is Recession Looming?” and answered in the negative. The present note sends a broadly similar message. A recession at some time in the future is, sadly, inevitable. There have always been recessions in the past and there will, unfortunately, be recessions again in the future. Western Europe, for instance witnessed six recessions since the early 1970s, one on average every 8 years. Since the last one was in 2012-13, this would suggest that the next one should hit in 2020-21. Arithmetic averages, however, do not have much scientific value. Hence the hope that the “inevitable” future recession will be postponed.

Many observers are particularly worried about the U.S. The economy has just entered the 121st month of expansion since the Great Recession of 2008-09 (the U.S. avoided the European debt recession of 2012-13), turning this upswing into the country’s longest. But clouds are gathering. The stimulus that came from Trump’s tax cuts in 2017 is quickly fading; protectionism is hurting some parts of the U.S. economy and eroding confidence; the housing market is relatively weak; and the yield curve has at times in the recent past inverted its profile (i.e. long-term interest rates have been below short-term ones), a signal that has regularly announced past recessions, etc. Yet, other indicators still suggest that there is some momentum left, with consumer spending in particular, quite buoyant. In addition, the fear that the Federal Reserve might raise interest rates, thereby depressing demand and hurting Wall Street, has clearly lifted. If anything, the next central bank move is very likely to be a cut in interest rates and this should bolster confidence and activity. A slowdown is inevitable; a recession is not.

In the emerging world, China is, of course, also slowing down, but its recent monetary policy relaxation should sustain a growth rate of the order of 5.5-6% per annum, hardly a sign of recession. Latin America is going through a bad patch (with its three largest economies, Argentina, Brazil and Mexico, seeing declines in output in the first quarter of this year) and may continue to tread water. Elsewhere, however, prospects are less gloomy. East Asia is being helped by China’s monetary relaxation, India keeps growing at relatively rapid rates (even if there is some doubt about the reliability of its statistics), Turkey’s sharp recession is now giving way to some recovery and East-Central Europe is still expanding rapidly.

The West European picture, not unlike the American one, is mixed. The manufacturing sector looks depressed. Industrial production has been flat or falling (year-on-year) in most countries since autumn; advance indicators, such as purchasing managers’ indices for the manufacturing sector, are suggesting that recessive conditions will continue to prevail in the coming months, especially in Germany and Italy, while world trade growth remains very sluggish. Residential construction seems also to be weakening. 2017-18 saw a moderate upswing in housing investment in the Eurozone, but this is now giving way to a slowdown. Growth rates are expected to remain positive in 2020-21 but might well settle at less than one percent in countries such as France or Italy. The only good news is that house prices are still rising steadily, if modestly, in most Eurozone countries (with the continuing exception of Italy).

A “hard Brexit” (an outcome whose likelihood is increasing) would also take its toll. Britain would, of course, suffer most, with GDP growth in 2020 reduced to zero or thereabouts (as against a forecast today of 1.5% based on the hypothesis of an agreement being reached between Brussels and London). Continental Europe, let alone Ireland, would also be hit. Simulations by Oxford Economics suggest that Eurozone growth in a “hard Brexit” scenario rather than being close to 1.5% in 2020 might be closer to one percent. Finally, Trump’s threats of protectionism against European exports create further uncertainty and dampen confidence.

Yet domestic demand and prospects for the service sector look more upbeat. Both are buoyed by continuing falls in unemployment and positive (if not spectacular) real wage growth. In addition, economic policies remain very accommodating. The European Central Bank’s most recent pronouncements suggest that a return to positive short-term interest rates may have to wait for 2021 and that a new bout of quantitative easing cannot be excluded should activity weaken further or inflation fail to rise. In anticipation, long-term bond yields have fallen to exceptionally low levels everywhere. On the fiscal front, Germany is relenting, if only at the margin, from its policy of seeking a large budget surplus. France, Italy and Spain all face Brussels-dictated constraints on their expansionary zeal, but some stimulus is bound to be forthcoming next year even if this risks breaking the limits imposed on budget deficits by the EU’s rules.

The overall situation, however, remains fragile. Global political uncertainties, particularly in the Middle East, could generate an oil price shock that might well send Europe into recession. A trade-war escalation between the U.S. and China could inflict significant damage. There is a truce at present in the trade conflict between the two countries, but this may not last given Trump’s unpredictability. And Trump may, of course, turn his attention to Europe instead, imposing, for instance, tariffs on automotive equipment exports to the U.S., as he has threatened to do on several occasions. This would add to the Eurozone’s problems, problems which, as often mentioned in the past, have not gone away. Italy remains in an exposed position even if the European Commission and the Italian government have, for the time being at least, moved away from a possible clash. And neither the U.S. nor Europe have at their disposal effective macroeconomic policy tools with which to offset any unfavorable shock. Falling interest rates in the U.S. and continuing negative interest rates in the Eurozone can help in sustaining activity, but their power to positively stimulate it is limited. Absent sudden negative shocks, a recession can be avoided, but relatively low growth (in the region of 1 to 1.5% per annum in Western Europe and North America) is here to stay.

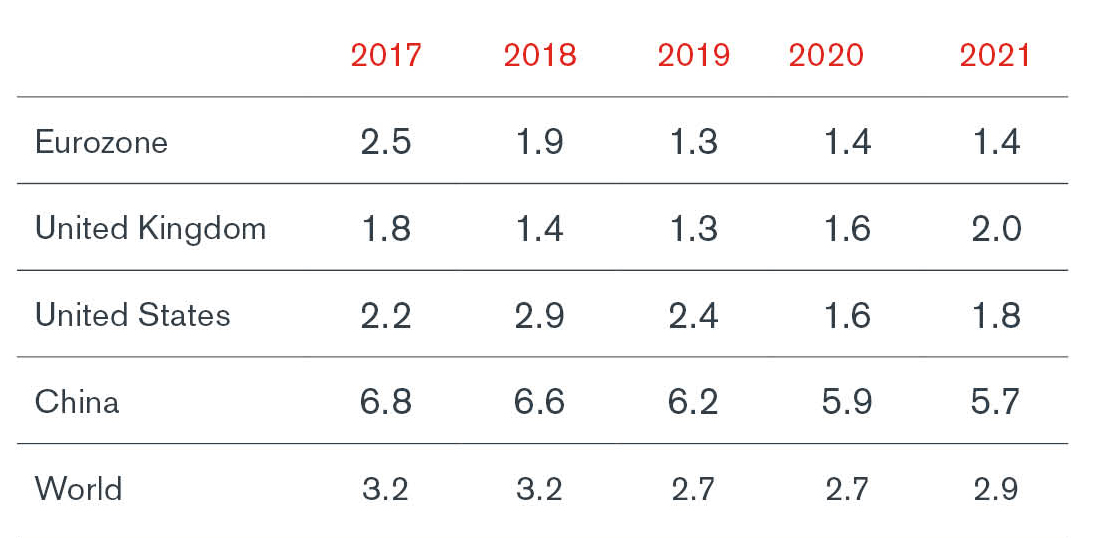

Source: Oxford Economics.

Duff & Phelps expressly disclaims any liability, of any type, including direct, indirect, incidental, special or consequential damages arising from or relating to the use of this material or any errors or omissions that may be contained herein.

Stay Ahead with Kroll

Real Estate Advisory Group

Leading provider of real estate valuation and consulting for investments and transactions.

Valuation Services

When companies require an objective and independent assessment of value, they look to Kroll.