As we look back at 2019, it’s important to highlight some of the headwinds that raised concerns across the U.S. and abroad: disruptive trade wars, a global economic slowdown, Brexit uncertainty, climate concerns, and political protests that reverberated through Hong Kong, Chile, Lebanon and several other places. Despite a sub-optimal backdrop, 2019 witnessed some of the biggest gains from stocks since 2013. The S&P 500 delivered a gain of more than 28%, which came close to reaching the 31% gain in 1997 and was a touch lower than the 30% return in 2013. Much of the gains in equities can likely be attributed to global monetary easing, with the Federal Reserve’s dovish pivot earlier in the year vs. the four rate hikes in 2018, as well as rising wages and continued low unemployment at 3.5%.

Although some of the headwinds from 2019 persist and are joined by new challenges such as the coronavirus, abundant capital continues to be the recurring theme for private equity and corporates. This will likely fuel M&A activity in 2020 as macroeconomic and political uncertainty stirs a sense of urgency to consummate transactions. Indicative of sustained investor interest in strong brands and concepts, we ended the year with continued momentum of transaction activity within the broader apparel and retail sectors. Highlighting a few of the deals that took place: Hurley was acquired by Blue Star Alliance, Revolve went public, and Louis Vuitton had an active year with its acquisition of Tiffany as well as a minority stake in Stella McCartney.

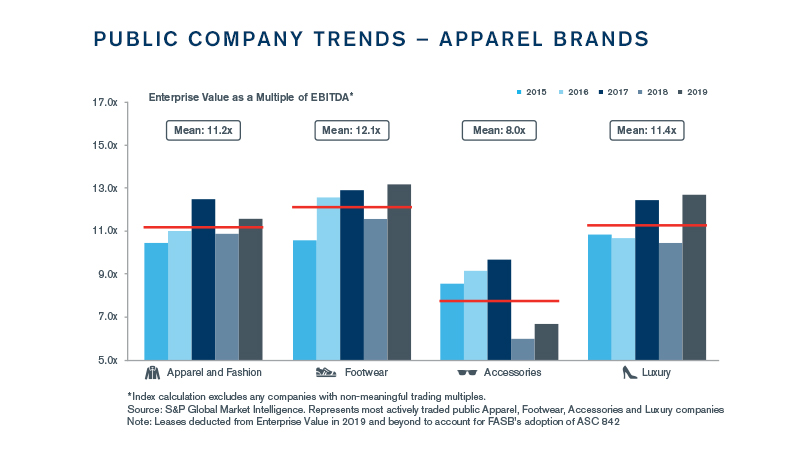

Valuations in the broader apparel and retail sectors inched upward and remained strong, with average LTM EV/EBITDA multiples of 11.0x and 10.3x, respectively. Comparing these levels to multiples in 2018 of 9.7x and 9.1x and the latest five-year average of 10.7x and 9.1x, we continue to see a premium being placed on strong, innovative brands with compelling customer value propositions. Within the apparel space, the active apparel sub-sector continued to garner the highest valuations at 14.6x. Online retailers led the pack at 20.1x within retail, and was closely followed by the off-price retail segment at 16.2x.

Our quarterly apparel report aims to identify trends and provide insights across the apparel sector, focusing on key themes, issues and opportunities. As sector spotlights in this issue, we address two key topics that have direct implications to the apparel and retail sectors: the upcoming U.S. presidential election and tariffs. We hope you continue to find this report and its future editions to be a useful source of information.

Connect with Us

Stay Ahead with Kroll

Mergers and Acquisitions (M&A) Advisory

Kroll’s top ranked M&A Advisory practice spans sell-side, buy-side, due diligence, deal strategy and structuring, and capital raising.

Consumer, Food, Restaurant and Retail Investment Banking

Consumer, Food, Restaurant and Retail expertise for middle-market M&A transactions.

Transaction Advisory Services

Kroll provides comprehensive due diligence, operational insights, and tax structuring support, assisting private equity firms and corporate clients throughout the deal lifecycle.

Transaction Opinions

Our Transaction Opinions solutions span fairness opinions, solvency opinions, ESOP/ERISA advisory, board and special committee advisory, and complex valuations.

ESOP and ERISA Advisory

Kroll's ESOP/ERISA practice is a leading corporate finance and valuation advisor to companies and ERISA fiduciaries.

Financial Sponsors Group

Dedicated coverage and access to M&A deal-flow for financial sponsors.

Distressed M&A and Special Situations

Kroll professionals have advised hundreds of companies, investors and other stakeholders at all stages of distressed transactions and special situations.

Debt Advisory

Kroll has extensive experience raising capital for middle-market companies to support a wide range of transactions.